Meeting the federal requirement to verify employment eligibility within 3 business days of hire

Executive Summary

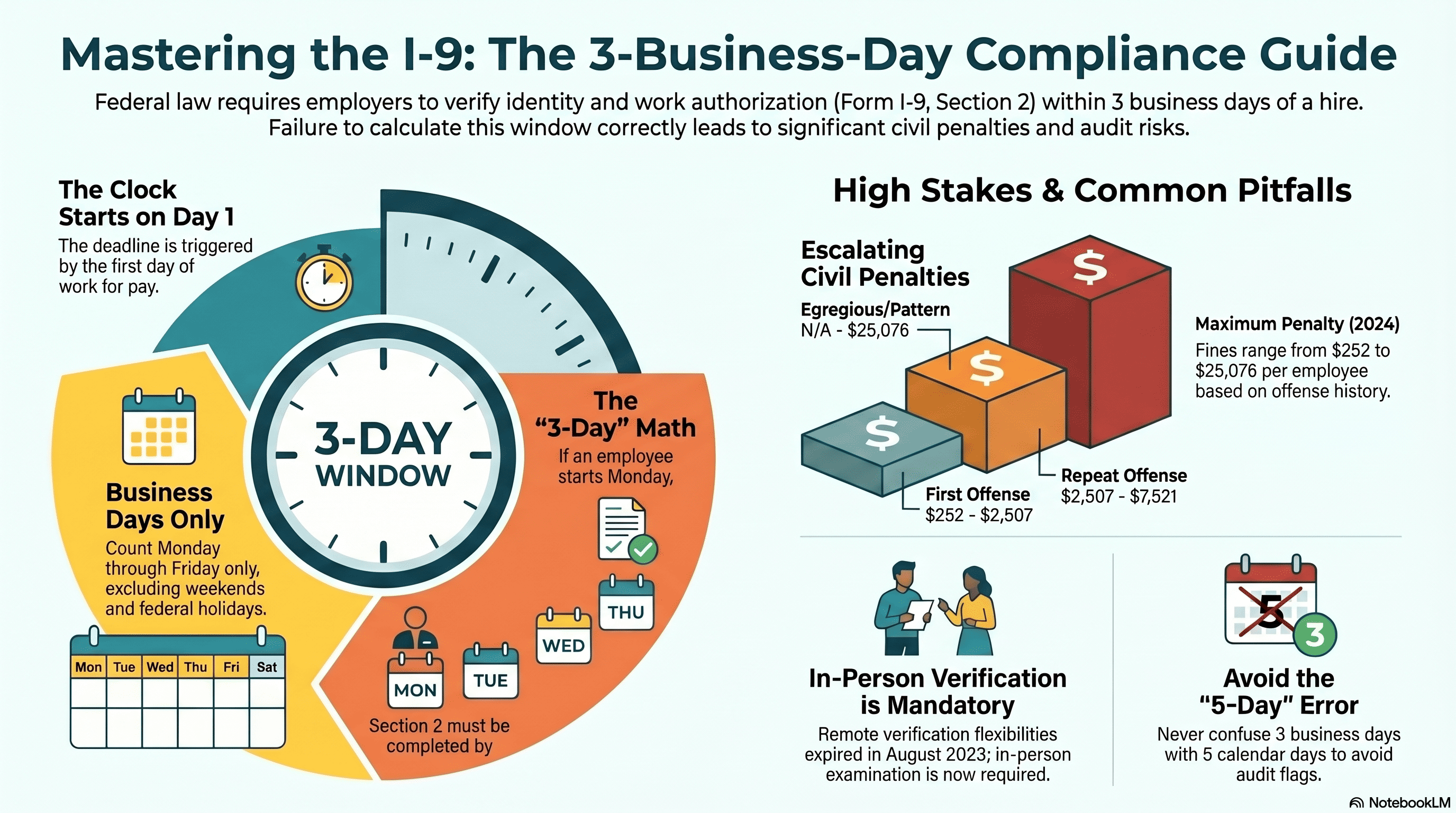

Federal immigration law requires employers to complete Section 2 of Form I-9 (Employment Eligibility Verification) no later than 3 business days after an employee’s first day of work for pay. This seemingly straightforward deadline creates substantial compliance risk: miscalculating what counts as a “business day,” misunderstanding when the clock starts, or missing documentation deadlines can result in civil penalties of $252 to $2,507 per violation on first offense—and up to $25,076 for repeat violations under 8 USC §1324a(b). The IRS has issued over 6,000 Notices of Inspection annually in recent years, making I-9 compliance one of the highest-impact areas for employment law risk. This article provides a forensic examination of the 3-business-day rule, remote verification procedures, practical workflow design, and common timing errors that trigger audits.

The Statutory Framework: 8 USC §1324a and DHS Regulations

The Immigration Reform and Control Act (IRCA), codified at 8 USC §1324a, establishes the foundational requirement that employers must examine an employee’s identity and employment authorization documents “within three business days of the hire date.” This statute has remained virtually unchanged since 1986, yet its application has evolved significantly with remote work adoption, E-Verify integration, and DHS guidance.

8 CFR §274a.2(b) implements this requirement and specifies that failure to complete Section 2 within the deadline constitutes a violation per employee. The regulation defines “3 business days” as any day Monday through Friday, excluding federal holidays. Critically, DHS explicitly states that weekend days and federal holidays do not count toward the deadline—a calendar-day calculation will always exceed the true business-day deadline and create false compliance gaps.

The statute also permits completion on the first day of work if the employee is examined on that date, though few employers structure hiring to accommodate this option. Understanding this statutory language is essential because penalties are assessed not per form or per violation, but per employee, meaning a single audit can result in substantial aggregate liability if timing errors are discovered across multiple hires.

Calculating the 3-Business-Day Deadline: When the Clock Starts

The first crucial determination is establishing the “hire date” for purposes of this calculation. The regulations state that the clock starts on the employee’s first day of work for pay—not the date the offer letter was signed, not the date the application was submitted, and not the date the conditional offer was made.

- First Day of Work for Pay = The Trigger: In most traditional employment relationships, this is straightforward: the employee works their first shift, and Section 2 must be completed by 5 p.m. on the third business day thereafter. However, the definition creates ambiguity in several common scenarios.

- Day 1 (First Work Day) + 3 Business Days: If an employee begins work on a Monday (Day 1), the deadline falls on Thursday of that same week (Days 2, 3, and 4 being Tuesday, Wednesday, and Thursday). If the employee begins work on a Friday, the deadline extends to Thursday of the following week because Saturday and Sunday are not business days, and then we count Monday, Tuesday, and Wednesday as business days 2, 3, and 4.

- Federal Holidays Stop the Clock: If a federal holiday falls within the 3-business-day window, that day does not count. For example, an employee who begins work on November 30 (Thursday before Thanksgiving) will have a deadline of December 2 (Monday after the holiday) because November 28–29 (Friday–Saturday before Thanksgiving) and November 27 (Thanksgiving) do not count as business days.

- Conditional Offers Do Not Start the Clock: A conditional offer of employment—even one that specifies “contingent upon I-9 verification”—does not start the clock. The employee must actually perform work and receive compensation for the clock to begin.

This distinction matters significantly for high-volume recruiting. When candidates receive conditional offers before completing the hiring process, the Section 2 deadline does not begin until the employee’s actual start date. Employers who conflate offer date with work-start date will incorrectly believe they have more time than they actually do.

Remote Verification and DHS Flexibility: The August 2023 Deadline

During the COVID-19 pandemic, the Department of Homeland Security implemented temporary flexibility allowing employers to conduct remote I-9 verification using video conferencing technology. This alternative procedure—detailed in DHS guidance issued in March 2020—permitted employers to verify documents electronically rather than in person, addressing operational constraints when offices were closed.

Critically, this temporary flexibility expired on August 15, 2023. DHS did not extend the remote verification procedures, and there is no indication that further extensions are planned. As of August 16, 2023, employers must conduct in-person examination of documents to complete Section 2, unless the employee is a remote worker who will have no in-person contact with the employer (in which case certain alternative procedures apply, but these are narrowly construed).

This shift creates significant compliance implications for organizations with distributed workforces. Employers cannot extend hiring start dates or claim “reasonable cause” for untimely completion based on inability to conduct remote verification. For remote workers, DHS allows examination conducted by a third-party inspector (such as a local notary public or HR service provider), provided the employer retains video or photographic evidence of the examination. However, the employer remains liable for verification accuracy—outsourcing the examination does not shift accountability.

Organizations that failed to complete Section 2 verification in person by August 31, 2023 for employees who began work on or after August 16, 2023 face retroactive violation liability. The August 2023 deadline created a significant audit risk for companies with incomplete transition plans.

Receipts, Temporary Documents, and the Completion Exception

Employees are sometimes unable to provide original identity and employment authorization documents on their first day of work. For example, a green card may be in transit, an employment authorization document (EAD) may be pending issuance, or original documents may be temporarily unavailable. Federal regulations provide a solution: employers may accept temporary documents or receipts issued by government agencies (such as a Social Security card receipt, receipt for a pending green card, or receipt for an EAD).

8 CFR §274a.2(b)(1)(vi) explicitly allows employers to complete Section 2 using a receipt that establishes the employee’s identity or employment authorization, so long as the employee provides the original document within a reasonable period (typically defined as within 60 days or earlier if possible, though the regulation itself does not specify a fixed deadline). When this occurs, Section 2 is still deemed “completed” for purposes of the 3-business-day deadline, and the receipt is recorded as the List A, B, or C document for the initial verification.

This receipt procedure is critical for high-volume hiring. An employer who hires 50 employees in a week and half lack documents may complete Section 2 for all 50 employees within the deadline by accepting receipts, provided there is a documented expectation that original documents will be provided. However, this procedure creates a secondary compliance obligation: the employer must follow up to collect the original documents and update the I-9 form once they are provided. Employers who accept receipts but fail to update the I-9s with original documents later face reverification violations and audit liability.

Best practice is to document in writing—via email confirmation or onboarding documentation—the receipt procedures and the deadline by which original documents must be provided. This creates a paper trail that demonstrates the employer’s good-faith compliance effort.

E-Verify Integration and the Completion Clock

Many employers use E-Verify—the Department of Homeland Security’s electronic employment verification system—to confirm employment eligibility. E-Verify integration does not change or extend the 3-business-day deadline for completing Section 2. However, E-Verify’s operational requirements can create practical complications that affect timing.

When an employer submits an I-9 to E-Verify, the system conducts an automated check of the employee’s information against Social Security Administration and DHS databases. Most cases resolve with an immediate “Employment Authorized” status. However, a subset of cases generate a “Case in Progress” status, which means DHS needs additional time to verify the information—typically 24 hours but potentially longer. During this “case in progress” period, the employee is technically work-authorized and may lawfully work, but E-Verify has not issued a definitive result.

The critical compliance question: if E-Verify shows “Case in Progress” at the point when the 3-business-day deadline arrives, is the employer in violation for not receiving a final E-Verify status? The answer is no. Section 2 is deemed completed when the employer has examined the documents and recorded them on the form, regardless of E-Verify status. E-Verify is a secondary verification tool, not a prerequisite for Section 2 completion. The employer should complete Section 2 within 3 business days, then submit to E-Verify to obtain a subsequent employment verification status. If E-Verify identifies discrepancies, the employer then follows the reverification procedures outlined in 8 CFR §274a.2(b)(2).

However, employers should not conflate “E-Verify submission” with “Section 2 completion.” These are separate obligations with different timelines. E-Verify submission should typically occur within the same 3-business-day window to minimize liability exposure, but the two are distinct actions.

Penalties for Violations and the IRS Audit Process

The penalty structure for I-9 violations under 8 USC §1324a(b) is designed to escalate with repeat violations. For employers with no prior I-9 violations, the civil penalty for each employee for whom Section 2 was not completed timely ranges from $252 to $2,507 per violation (2024 adjusted amounts; penalties increase annually). Employers with prior violations face penalties ranging from $2,507 to $7,521 per violation. For egregious violations or patterns of non-compliance, the penalty can reach up to $25,076 per violation.

These penalties are assessed per employee, not per form. An audit discovering timing violations for 20 employees could result in aggregate penalties of $5,040 to $50,140 for first-time violations alone. The IRS conducts approximately 6,000 Notices of Inspection (NOIs) annually, and ICE criminal investigations have increasingly prioritized I-9 audits at facilities with high-volume hiring.

The audit process typically begins with an ICE agent or Department of Labor investigator requesting the I-9 forms for a sample of current and former employees. The agency then examines whether Section 2 was completed within 3 business days of the hire date, whether all required fields were completed, and whether document examination was conducted by a person authorized to do so. The investigator constructs a timeline from the hiring records (offer letter dates, first pay stub dates, HR files) to establish when the employee’s “first day of work” occurred.

Crucially, the investigator has discretion to extrapolate violations discovered in the sample to the entire workforce. If violations are found for 10 percent of sampled employees, the investigator may assess the violation for the entire cohort, multiplying the penalty exposure dramatically. Employers without clear documentation of completion dates face heightened extrapolation risk because they cannot demonstrate that the violations found in the sample are anomalous.

When violations are discovered, the employer has a limited window to request mitigation based on “good faith” compliance efforts. This might include evidence of compliance training, established I-9 procedures, and isolated errors rather than systematic non-compliance. However, showing documents were not completed timely is difficult to defend as a good-faith error.

Practical Workflow Design to Ensure Timely Completion

Designing a hiring workflow that systematically meets the 3-business-day deadline requires coordination among HR, payroll, and hiring managers. The following framework addresses common failure points:

- Establish a Central I-9 Completion Point: Rather than allowing individual departments or hiring managers to schedule I-9 verification, designate a centralized HR team member or third-party administrator responsible for all Section 2 completions. This ensures consistent application of the 3-business-day rule and prevents variations based on location or department.

- Document the First Day of Work in Writing: When an employee is hired, the HR system should capture the first day of work for pay in a standardized field. This date should be clearly communicated to the I-9 coordinator so the deadline calculation is unambiguous. For conditional offers, explicitly note that the clock has not started until actual work commences.

- Schedule I-9 Verification on Day 1 or 2: Best practice is to complete Section 2 verification on the employee’s first day of work or the business day immediately following. This approach (1) ensures the deadline is met with margin for error, (2) allows receipt of documents from the employee at onboarding, and (3) creates clear operational discipline. If documents are unavailable, receiving receipts on Day 1 and scheduling follow-up for original documents within 60 days minimizes reverification risk.

- Implement Automated Deadline Tracking: Use HRIS or ATS systems with deadline tracking to flag any I-9 form not completed by the 3-business-day cutoff. The system should identify the deadline date and send reminders to the I-9 coordinator on Day 2 and Day 3 of the employee’s tenure.

- Document Verification Completion with Date and Signatory: Section 2 of the I-9 includes a line for the preparer’s signature and date. This signature and date should be completed and matched against the first day of work to create a clear record. For electronic I-9s, the system should log the completion timestamp automatically.

- Account for Federal Holidays in Threshold Planning: Maintain a current list of federal holidays and factor them into deadline calculations. If a federal holiday falls within the 3-business-day window, adjust the deadline accordingly. Some organizations use a simple formula: (First Day of Work + 3 business days) rather than (First Day of Work + 5 calendar days) to avoid miscalculation.

Common Timing Errors and Audit Red Flags

Years of ICE audits have identified recurring error patterns that trigger investigator scrutiny. Understanding these patterns allows employers to avoid them:

Calculating 3 Business Days as 5 Calendar Days: The most common error is counting Day 1 (first day of work) plus five calendar days. For example, if an employee starts on a Monday, some employers believe the deadline is Saturday (5 days later). In fact, the deadline is Thursday (Day 1 = Monday, Day 2 = Tuesday, Day 3 = Wednesday, Day 4 = Thursday). This miscalculation routinely results in I-9s completed on Saturday or Sunday—days on which the employer likely did not conduct the verification—or on a date that exceeds the business-day deadline. ICE auditors immediately flag I-9s with completion dates that fall outside the business week or that are dated after the calculated deadline.

Failing to Account for Holidays: Employers who fail to exclude federal holidays when calculating the deadline frequently miss their actual deadline. For example, an employee hired on the Thursday before Thanksgiving may have a deadline of Thursday of the following week (not the following Monday), because Friday of Thanksgiving week is not a business day. An employer who completes the I-9 on the following Monday will be one business day late. Documentation showing the deadline was miscalculated due to holiday oversight will likely result in violation assessment, though an employer may request mitigation if systematic compliance efforts are documented.

Separating Verification Date from Completion Date: Some employers conduct document verification on Day 1 but do not record the information on Section 2 until Day 5. While the verification itself occurred timely, the I-9 form was not completed until after the deadline. ICE distinguishes between the date documents were examined and the date Section 2 was prepared and completed. For audit purposes, the completion date (when Section 2 was signed) is the operative date. Employers should ensure verification and completion occur on the same date or within the same business day.

Missing or Undated Section 2 Completions: Approximately 20 percent of sampled I-9s in audits lack dates on which Section 2 was completed. Without a date, the employer cannot demonstrate the verification was timely, and the form is deemed non-compliant. Always include the completion date in Section 2.

How Cadient Talent SmartSuite Helps

Cadient Talent’s SmartSuite platform eliminates manual I-9 deadline tracking and calculation errors through automated workflow enforcement. The system automatically calculates the 3-business-day deadline based on each employee’s actual first day of work for pay, accounts for federal holidays in real time, and sends deadline reminders to designated I-9 coordinators. SmartSuite integrates with payroll systems to confirm work start dates, ensuring the deadline calculation is tied to actual compensation events rather than hiring dates. For organizations using remote verification procedures, SmartSuite maintains audit-ready video and document evidence, timestamped automatically. The platform also tracks receipt procedures and flags open reverifications due after 60 days, preventing the secondary violation of failure to update I-9s with original documents. By removing manual calculation from the I-9 process, SmartSuite reduces penalty exposure and audit liability while accelerating high-volume hiring.

References and Further Reading

- 8 USC §1324a(b): Civil penalties for I-9 violations (up to $25,076 per violation for repeat offenses)

- 8 CFR §274a.2(b)(1): Employment eligibility verification requirements and 3-business-day deadline

- 8 CFR §274a.2(b)(1)(vi): Acceptance of receipts and temporary documents

- 8 CFR §274a.2(b)(2): Reverification procedures when employee work authorization expires

- Form I-9 Instructions (2024 Edition): Completion timeline and document requirements

- DHS Immigration Reform and Control Act (IRCA) Penalties: 8 USC §1324a(e)–(h)

- ICE ERE Program: Employment verification guidance and audit procedures

- E-Verify Handbook: Integration with I-9 process and case resolution procedures

- Federal Holiday Schedule (OPM): 2024–2026 federal holidays affecting business-day calculations

How Cadient Talent SmartSuite™ Helps

Cadient Talent’s SmartSuite™ platform automates compliance workflows, embeds regulatory guardrails directly into your hiring process, and maintains audit-ready documentation at every stage—so your team can focus on finding great talent while staying protected from costly violations.